What is NHG? And am I eligible for it?

What is NHG?

NHG stands for Nationale Hypotheek Garantie, that translated means national mortgage guarantee.

It’s a national depot through which the government acts as guarantor for people asking a loan to a bank. By doing so, people can access mortgages at subsidized rates. However, this is restricted to certain requirements of the potential debtor and of the amount this person is going to require.

I will shortly touch on the eligibility criteria, the procedure to get it (and what are the costs of it) and finally I’ll try to give an idea of when it becomes advantageous with an example.

What are the eligibility criteria for NHG?

Normally the discussion about eligibility for NHG is done at the bank with your consultant. However, going prepared is always a good idea (in our specific case, that made having NHG possible).

There are two main aspects that play a role in the decision about NHG

- The amount you are requesting in the mortgage

Subsidized mortgage rates are meant for people with limited financial possibilities, and are thus not meant for luxury amounts (and houses).

There exists a threshold on the required amount for loan: if this value is below that specific threshold, then you satisfy the first condition.

In 2020, such threshold is 310.000 euro.

Note that this condition and threshold are connected with the required amount, and it can be thus associated with the cost of the house (also if brand new building), the renovation or both. However, the added value of renovation needs to be quantified by an independent appraiser (taxateur) before and after the work is performed, and also by a technical check.

Also for the house, if the value you are asking is much higher than the objective value estimated by the appraiser (taxateur), you won’t be able to get it.

If your plan includes also renovation for energy saving, then you’ll be able to get up to 328.600 euro.

In short: the amount you are requiring for both the house and its renovation together should not exceed the threshold (i.e. 310000 euro in 2020). - The type of contract of the applicant(s)

The second touches upon the financial stability of the applicants.

The mortgage itself requires a certain income from the applicants, but NHG adds a limitation on top of that. Permanent employment contracts give almost immediately right to get the subsidized mortgage rate, while for other type of contracts it is more complex.

If you (or partner) have a fixed-term contract, they’ll check the past years: if you have worked in the Netherlands for more than four years, they will take that into account, and estimate your income as the average over the last four years.

If you (and/or your partner) are self-employed, and you have already been active for at least 12 months, then you are also eligible for NHG. This in particular has been changed in January 2019, in order to give more/better chances of getting a mortgage to self employees.

This is an extremely simplified version of the complete requirement.

I suggest you in any case to have a look at the NHG website (they also have an English summary).

Note that both requirements above need to be fulfilled in order to be eligible for NHG.

How does NHG work?

- Discuss your eligibility to NHG with your (potential) creditor – a bank or financial advisor

- If you are eligible for NHG, your advisor will make you a contract under that condition

- The advisor him/herself will apply for NHG (thus you just need to take care that the eligibility is checked properly and that the conditions in your contract are the ones discussed)

- At the notary’s office (referring to the last step in the procedure explained in the previous post HOWTO. Buy a house in NL?), you’ll also transfer 0.7% of the required amount to the NHG via the notary. This guarantees your subsidized rate for the whole duration of the mortgage (also when the rate is fixed at 10 years. After 10 years, you’ll re-discuss the mortgage rate, but you’ll still be able to enjoy the reduced rate).

- You will get the NHG certificate some time after the notary appointment (in our case it arrived more than four months after).

Is it convenient?

Since there’s an initial ‘investment’ and the rate reduction is not extreme, you may wonder whether it is convenient to ask for the NHG, even without addressing whether you are eligible for it. But do not forget the rate reduction is small over large amounts – see the example below to get an idea.

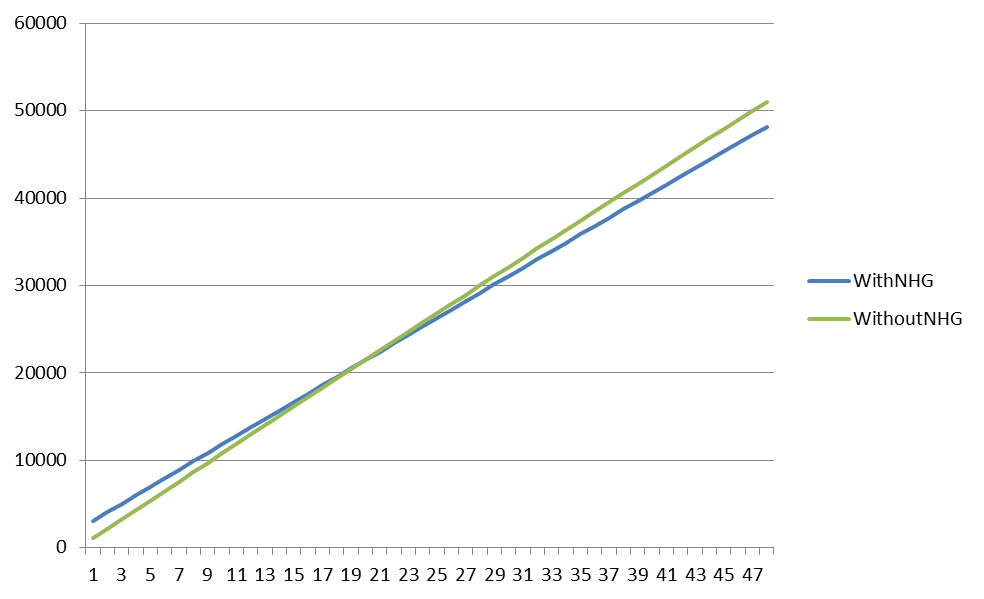

Imagine you are buying a house that costs 300.000 euro, and you have no finances to support this purchase. You’re therefore asking a mortgage for the whole amount (without any renovation). Let’s also assume the objective estimated value of the house is also 300.000 euro and you’re eligible for NHG. Finally, we’ll take likely values for the mortgage rates fixed at 10 years

with NHG = 1.29% + fixed initial cost of 2100 euro (=300000*0.7%)

without NHG = 1.72%

In the plot I show the cumulative monthly costs for the mortgage – including interests and return of mortgage, and the initial costs for NHG – per month.

You can see that already before the end of the second year (before the 24th month), the NHG makes you save money. It may not seem a lot, but the scale is quite large: look at how many zeros there are! And the horizon plotted here is just up to four years. You can extend the lines to see where you will end up after 10 years.

Other advantages

Even more importantly, NHG will help you in case your financial situation changes (like you loose the job, you end the relationship with the person you had the mortgage with or such), and you are no longer able to pay the monthly costs. Instead of forcing you to directly sell the property, they support you in this difficult situation and possibly allow you to keep the house, helping you to go through this moment.

In short, I think this is a pretty decent deal unless you plan to resell the house really in short term. Note also that this computation does not take into account the fact that the costs linked with the NHG are deductible!

Did you know what NHG is? Planning to request it now?

Doei!

Marta

Related Posts

Comparison of mobile sim-only contracts (with freebie!)

2020 – Public and school holidays in the Netherlands (with free calendar)

Which supermarket is the cheapest? (2018)

How to exchange your foreigner driving license to a Dutch one? (EU/EFTA)

Discounts for train tickets in NL: 4 easy ways to save money

Which supermarket is the cheapest? Picnic vs AH and Jumbo

First aid to buy medicines

Buying a house in NL. How much does it cost?

Add a Comment

You must be logged in to post a comment.

One Response